Moved all my OA monies I received whilst working previously to my SA.

Reason being I won't be buying a HDB flat with it in the foreseeable future (at least the next 5-8 years) and the difference in interest rates would mean quite a difference in the compounding effect.

Anyway, the sum won't mean much in buying a flat. Less than 1% of a new 4-room flat.

Friday, November 11, 2011

Wednesday, September 28, 2011

Unable to post for the time being

I have been extremely busy with school and settling in that I feel I will not have much time to post for the foreseeable future. Thanks to all readers and commenters thus far.

Friday, September 9, 2011

Divested Mapletree Industrial

Queued and sold MIT at $1.195 today, giving about a 25% profit after accounting for dividends.

Sold as it's approaching resistance at 1.20 and I'm betting that the downside risk is much more than the upside potential at current prices. Hence, decided to take profit off the table.

At $1.20 MIT's yield is at 6%, commensurate with A-REIT but with higher gearing. Thus I think MIT has gone a tad over-valued.

There are better deals out there and I will be looking to put some capital into other counters should their prices fall and value emerge.

Sold as it's approaching resistance at 1.20 and I'm betting that the downside risk is much more than the upside potential at current prices. Hence, decided to take profit off the table.

At $1.20 MIT's yield is at 6%, commensurate with A-REIT but with higher gearing. Thus I think MIT has gone a tad over-valued.

There are better deals out there and I will be looking to put some capital into other counters should their prices fall and value emerge.

Thursday, September 8, 2011

ST Engineering: Analyst report

Protect your portfolio! This should be the best time to buy STE for its defensive

quality in the face of volatile markets. Indeed, its share price has outperformed the

market by 11% in the last three months. With little room for sharp depreciation in

the US$, we are hanging on to hopes of earnings surprises, which we believe can

offer re-rating catalysts. Consensus expects the US$/S$ to hover at S$1.18-1.20

into 2012, which would have a negligible (1% or S$6m) impact on STE’s PBT in

the worst case. In fact, we believe current valuations of 15x CY12 P/E (below its

average trading band of 16x during the previous crisis) have priced in fears of US$

deterioration and macro uncertainties. No change to our earnings estimates, target

price of S$3.61 (still based on blended P/E, DCF and dividend yields).

• Zero order-book risk. Unlike its conglomerate peers with substantial exposure to

the offshore & marine space, STE’s order book (S$10.8bn) is secure with almost

zero risk of cancellations as 40-50% of its contracts are defence-related.

Commercial contracts are mostly from long-term customers with strong financials

including Fedex, American Airlines and Japanese airlines. STE has also been

chalking up orders from all segments worth about S$1.5bn YTD.

• MRO recovery intact. More than 1,500 narrow-body aircraft (delivered in 2009-

2010) could be scheduled for “C” checks (18-24-month cycle) starting 2H11,

affirming our view that the MRO recovery is on track.

• High yields and cash-rich. STE offers a safe refuge with its fairly attractive

dividend yields of about 6%, only slightly lower than the 7% from telcos and REITs.

The yield is also backed by a solid balance sheet as it continues to generate net

cash (S$220m as of 1H11). It is also one of two companies in Singapore with an

AAA rating (the other being Temasek) from Moody’s.

Unscathed. This should be the best time to buy STE for its defensive quality in the face

of volatile markets. Indeed, its share price has outperformed the market by an average

of 11% in the last three months while other offshore & marine/conglomerate stocks are

down about 10% relative to the market. We believe a solid balance sheet with a netcash

position, a secure order book and below historical average trading valuations

could be its winning factors.

Taken from here

I didn't know ST Engineering was a AAA rated company alongside Temasek.

Funny that analysts should start praising ST Engineering for it's defensiveness now. I would have thought that all counters will drop in a bear market. Maybe, he who drops least, wins. lol!

Again, it all boils down to one's money management.

quality in the face of volatile markets. Indeed, its share price has outperformed the

market by 11% in the last three months. With little room for sharp depreciation in

the US$, we are hanging on to hopes of earnings surprises, which we believe can

offer re-rating catalysts. Consensus expects the US$/S$ to hover at S$1.18-1.20

into 2012, which would have a negligible (1% or S$6m) impact on STE’s PBT in

the worst case. In fact, we believe current valuations of 15x CY12 P/E (below its

average trading band of 16x during the previous crisis) have priced in fears of US$

deterioration and macro uncertainties. No change to our earnings estimates, target

price of S$3.61 (still based on blended P/E, DCF and dividend yields).

• Zero order-book risk. Unlike its conglomerate peers with substantial exposure to

the offshore & marine space, STE’s order book (S$10.8bn) is secure with almost

zero risk of cancellations as 40-50% of its contracts are defence-related.

Commercial contracts are mostly from long-term customers with strong financials

including Fedex, American Airlines and Japanese airlines. STE has also been

chalking up orders from all segments worth about S$1.5bn YTD.

• MRO recovery intact. More than 1,500 narrow-body aircraft (delivered in 2009-

2010) could be scheduled for “C” checks (18-24-month cycle) starting 2H11,

affirming our view that the MRO recovery is on track.

• High yields and cash-rich. STE offers a safe refuge with its fairly attractive

dividend yields of about 6%, only slightly lower than the 7% from telcos and REITs.

The yield is also backed by a solid balance sheet as it continues to generate net

cash (S$220m as of 1H11). It is also one of two companies in Singapore with an

AAA rating (the other being Temasek) from Moody’s.

Unscathed. This should be the best time to buy STE for its defensive quality in the face

of volatile markets. Indeed, its share price has outperformed the market by an average

of 11% in the last three months while other offshore & marine/conglomerate stocks are

down about 10% relative to the market. We believe a solid balance sheet with a netcash

position, a secure order book and below historical average trading valuations

could be its winning factors.

Taken from here

I didn't know ST Engineering was a AAA rated company alongside Temasek.

Funny that analysts should start praising ST Engineering for it's defensiveness now. I would have thought that all counters will drop in a bear market. Maybe, he who drops least, wins. lol!

Again, it all boils down to one's money management.

Wednesday, September 7, 2011

UK Pound Sterling against Singapore Dollar

Period of extreme volatility in the forex markets too. Pound Sterling and Euro have declined precipitously against the Singapore Dollar as I write this. Pound to 1.929 and Euro to 1.69. The former is a historical low (yet again), the latter is not too far away from it's historical low at 1.55-ish.

Swiss National Bank has also publicly stated it will intervene in the forex markets to keep EUR/CHF at a maximum of 1.20, which led to EUR/CHF to drop to... you guessed it... 1.20. It's also dropped to 1.40 against the Singapore Dollar.

Interestingly enough, the US dollar has risen against the Singapore dollar. Now stands at 1.211.

Long term prognosis for these beleaguered western currencies? Heal, relief or comfort? I have no idea, but it doesn't look too good. As far as I know, currency exchange rates in the long term are very based on macroeconomics.

Let me try my hand at this.. In a fictional world with two countries only, A and B:

1.) If A's inflation rate is 4% whilst B's is 6%, ceteris paribus, A's currency will strengthen against B's.

2.) Again, if country A's money supply rises slower than B's, ceteris paribus, A's currency will rise against B's. This is because B has essentially more numbers chasing after the same amount of goods.

3.) If country A's interest rates are higher vis a vis country B's, ceteris paribus, A's currency will strengthen against B's.

4.) If country A's current account deficit is bigger vis a vis country B's, ceteris paribus, A's currency will decline against B's. This is because A owes B more money than B owes A. Hence, A has to supply the market with more A$ to buy the limited supply of B$. Supply of A$ increases, Demand for B$ increases, B$ appreciates.

5.) If country A's government is constantly facing unrest and hostility whilst B's government is keeping the peace, B's currency will rise vis a vis A's.

6.) If country A's public debt is bigger as compared to B's, A's currency will decline. This is because a large debt encourages inflation, which brings us back to point 1.

7.) Market Sentiments (duh)

8.) Expected Central Bank actions w.r.t. interest rates, money supply easing etc

Look at Britain vis a vis Singapore. Point 2, 4, 7 and 8 I believe are to blame for this decline.

The sun never sets on the British Empire? Hmm....

But you know what? This is GREAT! This leads to lower cost of education for me, and a cheaper European holiday for my fellow countrymen. Majulah Singapura!

Wednesday, August 31, 2011

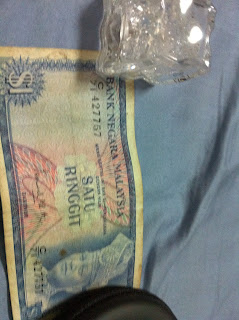

Banknotes & what I spent with my dividends

Had an interesting discussion on banknotes today. Went to raffles place today to change some money, some for myself and some for a family member.

In Europe, the 2 major currencies ( Euro + Pound) only issue relatively high value banknotes (i.e. starting from EUR5/GBP5) whereas in America, Brazil, China, Singapore, HK, Malaysia etc issue low denomination banknotes (e.g. US$1, RMB5, S$2, HK$10, RM1). It's pretty weird, for you'd probably end up with alot of change and loose coins when one visits Europe.

Some currencies are really weird however, like the US dollar. case in point:

Every denomination is of the same dimension and color. I wonder how their blind people know which is which. Imagine if you get mistaken and want to tip someone US$1, and end up tipping him US$100 because you thought it was US$1 :P

Every denomination is of the same dimension and color. I wonder how their blind people know which is which. Imagine if you get mistaken and want to tip someone US$1, and end up tipping him US$100 because you thought it was US$1 :P

As for the pound, this is it...4 banknote denomination in circulation. the £50 note is huge... around the same size as our S$1000 note.

As for the pound, this is it...4 banknote denomination in circulation. the £50 note is huge... around the same size as our S$1000 note.

Some of my old/interesting Singapore notes. I wonder why Singapore doesn't introduce a bona fide S$20 note.

Some Chinese notes I have. The "yi jiao" is RMB 0.10. Sing dollar 0.2 cents.

Egyptian pound

I also received MIT + First REIT dividends. Used part of the dividends to buy a nice silk tie on offer :D

usual price $53, bought for $19 from G2000 :)

In Europe, the 2 major currencies ( Euro + Pound) only issue relatively high value banknotes (i.e. starting from EUR5/GBP5) whereas in America, Brazil, China, Singapore, HK, Malaysia etc issue low denomination banknotes (e.g. US$1, RMB5, S$2, HK$10, RM1). It's pretty weird, for you'd probably end up with alot of change and loose coins when one visits Europe.

Some currencies are really weird however, like the US dollar. case in point:

{kind=link}

Some Chinese notes I have. The "yi jiao" is RMB 0.10. Sing dollar 0.2 cents.

Egyptian pound

I also received MIT + First REIT dividends. Used part of the dividends to buy a nice silk tie on offer :D

usual price $53, bought for $19 from G2000 :)

Wednesday, August 24, 2011

Mapletree Industrial Trust-PO results

As said in an earlier post, I applied for my entitlement and also for excess rights to make up the full board lot.

Just checked my CDP internet account and realized my excess application was successful. I was rounded up to a full board lot! Great, for it would have been an irritant to deal with odd shares.

Just checked my CDP internet account and realized my excess application was successful. I was rounded up to a full board lot! Great, for it would have been an irritant to deal with odd shares.

Monday, August 22, 2011

Singapore Technologies Engineering- Bucking the trend

Will I sell? Short answer, no.

Why? ST Engineering is a STI component, for the most part, it will follow the trend of STI. It's never good to be either fully invested nor fully divested. I'm currently at around 60-70% cash, with my holdings (in order of liquidation value marked to market): ST Engineering, First REIT, MIT, Sabana REIT. I will be holding on, sinking or swimming with these 4 counters. Potential downside is 50% or more (remember, ST Engineering went down to high $1+ in 2009), but as I have the holding power, I will just hold on for dividends, considering I bought this at a low price. Same goes for the three other REITS.

Tuesday, August 16, 2011

applied for MapletreeInd PO + Excess

Stopped by the ATM to apply for the MIT PO of 2 for 25 and applied excess to round up to full lot.

Fingers crossed that I'll be allotted excess units to make up 1 lot.

New units start trading on 24th August.

Fingers crossed that I'll be allotted excess units to make up 1 lot.

New units start trading on 24th August.

Wednesday, August 10, 2011

Sold off Poh Tiong Choon Logistics

Sold off PohTC at $0.400 today, making a loss of 10% after dividends.

Reasons:

1.) My original reason for buying was because of the huge insider buy ups. This was a punt for a privatization offer or something of the sort

2.) PohTC is very cyclical and unfortunately I think I bought at the peak cycle.

3.) I don't like the low liquidity

4.) I think there is alot more downside to the stock market, better clear off some non performers to get ready to buy from a bear market.

I will be interested to buy PohTC again, in a bear market, with SCB (I had to sell down just now, I didn't want to run the risk of a partial fill). Definitely not at this price though.

I will be looking to sell off other counters, at the right price. If not, I'm about 65% to 70% cash now anyway, and will hold on.

Won't be selling ST Engineering, this one is for keeps. Am looking to sell off First REIT at 80c and above, and am looking to buy at around 72c or so. Also looking to sell MIT. Target buys include Sabana REIT, SPH, ARA, SingPost, SMRT, SingTel. Obviously don't have many bullets so will have to pick and choose, so just wait and see who reaches target price first. Will be buying slowly.

Reasons:

1.) My original reason for buying was because of the huge insider buy ups. This was a punt for a privatization offer or something of the sort

2.) PohTC is very cyclical and unfortunately I think I bought at the peak cycle.

3.) I don't like the low liquidity

4.) I think there is alot more downside to the stock market, better clear off some non performers to get ready to buy from a bear market.

I will be interested to buy PohTC again, in a bear market, with SCB (I had to sell down just now, I didn't want to run the risk of a partial fill). Definitely not at this price though.

I will be looking to sell off other counters, at the right price. If not, I'm about 65% to 70% cash now anyway, and will hold on.

Won't be selling ST Engineering, this one is for keeps. Am looking to sell off First REIT at 80c and above, and am looking to buy at around 72c or so. Also looking to sell MIT. Target buys include Sabana REIT, SPH, ARA, SingPost, SMRT, SingTel. Obviously don't have many bullets so will have to pick and choose, so just wait and see who reaches target price first. Will be buying slowly.

Friday, August 5, 2011

-531, -112, -938

Tuesday, August 2, 2011

Payable dates for my counters

for own reference:

First REIT- 29th Aug

Sabana- 6th September

PM Data- 26th Aug, XD 11 Aug

ST Engg- 2nd Sept, XD 11 Aug

PohTC-TBA

MIT- 31st Aug, must remember to apply for PO and excess rights when the instructions come

First REIT- 29th Aug

Sabana- 6th September

PM Data- 26th Aug, XD 11 Aug

ST Engg- 2nd Sept, XD 11 Aug

PohTC-TBA

MIT- 31st Aug, must remember to apply for PO and excess rights when the instructions come

Wednesday, July 27, 2011

Median Income of the different professions in Singapore part 1

Business Times and Straits Times had an article a few weeks back regarding this issue.

I can't find the original article online, but if anyone has a BT subscription could kindly help me find it.

According to the department of statistics, the gross median income by profession are:

First figure is basic and second figure is gross:

1. Managers (including MD and CEO) 6,000 / 6,300

2. Professional (including doctors/lawyers/fund managers) 4,000 / 4,300

3. Associate professional & technicans 2,600 / 2,987

4. Clerical support workers 1,850 / 2,001

5. Service & sales workers 1,320 / 1,788

6. Craftsmen & related trades workers 1,790 / 2,250

7. Plant & machine operators & assemblers 1,380 / 1,896

8. Cleaners, labourers & related workers 850 / 960

MD and CEO topped the pay ranking, with a median gross salary of $14,765 monthly. That is more than what doctors ($10,786) and lawyers ($8,750) were paid.

(kindly taken from Ben's post here at ValueBuddies)

I also took the liberty to go through the Ministry of Manpower's site to find information on Mean & Median Income by profession. Not easy to find... but it's here. Frustrating enough to find, but even more frustrating after seeing they only show a few professions.

On face value, the lower remunerated blue collar jobs seem quite accurate, i.e. gross median wages of S$1,000 to S$2,500. However, I find certain jobs remuneration to be quite questionable, e.g. Dentists' median wage of S$4,000. (really meh?)

Will continue in a further post if I can find that article. I don't want to shoot off unsubstantiated figures.

I can't find the original article online, but if anyone has a BT subscription could kindly help me find it.

According to the department of statistics, the gross median income by profession are:

First figure is basic and second figure is gross:

1. Managers (including MD and CEO) 6,000 / 6,300

2. Professional (including doctors/lawyers/fund managers) 4,000 / 4,300

3. Associate professional & technicans 2,600 / 2,987

4. Clerical support workers 1,850 / 2,001

5. Service & sales workers 1,320 / 1,788

6. Craftsmen & related trades workers 1,790 / 2,250

7. Plant & machine operators & assemblers 1,380 / 1,896

8. Cleaners, labourers & related workers 850 / 960

MD and CEO topped the pay ranking, with a median gross salary of $14,765 monthly. That is more than what doctors ($10,786) and lawyers ($8,750) were paid.

(kindly taken from Ben's post here at ValueBuddies)

I also took the liberty to go through the Ministry of Manpower's site to find information on Mean & Median Income by profession. Not easy to find... but it's here. Frustrating enough to find, but even more frustrating after seeing they only show a few professions.

On face value, the lower remunerated blue collar jobs seem quite accurate, i.e. gross median wages of S$1,000 to S$2,500. However, I find certain jobs remuneration to be quite questionable, e.g. Dentists' median wage of S$4,000. (really meh?)

Will continue in a further post if I can find that article. I don't want to shoot off unsubstantiated figures.

Monday, July 25, 2011

The World's Most Expensive Cities For Expats

According to this article on http://www.forbes.com/2010/06/28/most-expensive-cities-lifestyle-travel-expats.html , Singapore has become the 8th most expensive place to live in in the world. Interestingly enough, Luanda in Angola is number 1?!?!

Monday, July 18, 2011

Noble: trading idea

Channel support broken. Can't say decisively yet it looks too out to be a whipsaw.

MACD potential bullish divergence negated with today's sharp downtick of both MACD line and histogram.

Next support at 1.67 then 1.57. Might get my foot in at 1.67 and add more at 1.57 should it be tested. Cut loss will be decided should noble get into my buy range.

profit target will be at channel support turned resistance, and then in the value zone between 13 and 21 day ema

Friday, July 15, 2011

Johor Bahru

Been going to JB alot recently. Friend drives and so we go for makan, shopping and movies.

The whole premise of JB is that we'd spend less because of the favourable exchange rate.

How ironic that we end up spending more by buying durians, groceries, watching movies, eating cze char by the bucketload.

Can this be said the same of commission charges? With SCB, I've seen people making more reckless trades as the commissions are much lower. Eventually, what is premised to be a money saving exercise actually cost people more in losses....

The whole premise of JB is that we'd spend less because of the favourable exchange rate.

How ironic that we end up spending more by buying durians, groceries, watching movies, eating cze char by the bucketload.

Can this be said the same of commission charges? With SCB, I've seen people making more reckless trades as the commissions are much lower. Eventually, what is premised to be a money saving exercise actually cost people more in losses....

Wednesday, July 6, 2011

Dapai International- postponing/?Canceling rights issue.

"The Directors wish to update Shareholders that the Company has had discussions with the

Singapore Exchange Securities Trading Limited regarding the proposed Rights Issue exercise and

understood that as the proceeds of the Rights Issue are intended to be used for a proposed

acquisition for which no agreement has been signed as yet and which when signed, will require

shareholders' approval, it is therefore pre-mature for the Company to carry out the proposed Rights

Issue exercise at this stage.

In view of the foregoing, the Company will postpone its plans for the proposed Rights Issue exercise

and will update Shareholders accordingly by way of announcement when and should it decide to

proceed with the rights issue exercise again."

Singapore Exchange Securities Trading Limited regarding the proposed Rights Issue exercise and

understood that as the proceeds of the Rights Issue are intended to be used for a proposed

acquisition for which no agreement has been signed as yet and which when signed, will require

shareholders' approval, it is therefore pre-mature for the Company to carry out the proposed Rights

Issue exercise at this stage.

In view of the foregoing, the Company will postpone its plans for the proposed Rights Issue exercise

and will update Shareholders accordingly by way of announcement when and should it decide to

proceed with the rights issue exercise again."

Thursday, June 30, 2011

British Pound-sliding against the Singapore Dollar

As some of you might know, I am going to the UK to further studies. I've been doing the carnal sin of traders: Averaging down on the GBP. (at 2.06, 2.01 and 1.98)

Interesting conundrum I have here: Every time the pound drops, I theoretically lose money but am happier, because the cost of my education is dropping.

A friend of mine has said he'll visit the UK when the pound exchange rate reaches 1.8. I hope it goes there too :)

Saturday, June 25, 2011

Stocks and Durians-yummy!

I like Durians. Love eating them, though I do so moderately, not because of any health aspects but more because they're pretty expensive.

I see quite a parallel between durians and the stock market.

In trying to bottom pick, we pick durians from the ground. Just don't stand under the durian tree too often; we might get knocked by the thorny durians on the way down...

In value investing, people scrutinize the business, it's financials, and it's valuations. Same for durians. If one wants to buy durians, he will scrutinize it, shake it, look at the color, look at the stem, check if the thorns are sharp and fresh. Lastly, having concluded that the durian is acceptable, we look at the price. Sometimes, durians are in large supply and we can get top grade durians at $10/kg. Sometimes, they are in short supply and cost $22/kg. So, we make a decision based on the current valuation whether to buy. If one deems it to be a value buy, we buy it at whatever Mr. Durian Seller/Mr. Market offers to us. If not, we just walk away, our banknotes safe and sound in our pockets.

We also can shop around. Stall A might be famous for it's Mao Shan Wang, but what if one wants to eat D24? Do we blindly go to Stall A? Sometimes, Stall B, which might not be famous for any cultivar, might offer D24 at cheaper prices. Same thing, we must also shop around for whoever lowers our cost. Sometimes, Stall A customers look down on Stall B customers because Stall B doesn't have a reputation. But, what matters is just the quality of the durians, no? Whether Stall A gives you aircon, more friendly staff, does it matter? I detect alot of snobbery and people turning their noses up at Standard Chartered Bank's offer of 0.20% commission with no minimum. Even though SCB might carry a bigger advantage for small players, people actually will save more when they trade more. If I want to buy $40,000 worth of ST Engineering, my commission for a traditional broker is at 0.275% which is $110+ gst. For SCB, that will be 0.20% which is $80+ gst. Of course, there are many other factors to look into; but I feel that the vibe of disdain and ridicule of SCB customers I get is unwarranted.

For durians, we must also know which cultivars are in season at the time we want to buy, which will offer us the best value for money. Say, in April, D24 from pahang is in season. We will get better value for money for D24 from Pahang in April, than say Mao Shan Wang from Perak. Sometimes, a flood/drought/whatever affects the whole South East Asia region and all durian trees, no matter how good, churn out poor quality durians. Same thing, we should look at the macro events and not just the business fundamentals of a stock. No matter how good a business is, a rising tide lifts all ships, and vice versa, a sinking tide grounds all ships. Even if a company is getting exceptional economic moat, ROE, ROI etc etc, a global economic downturn will sink it's stock price, will it not?

After all is said and done, when we bring the durian back, no matter how good it looked before we opened it, after opening, if there are worms inside, do we hold on to the durian hoping the worm will magically disappear, or do we take decisive action to throw the durian away before the worm replicates and goes into our other durians, or start to affect us?

That's my parallel of durian eating and stock picking. Enjoy both eating durians and picking stocks. Cheers!

I see quite a parallel between durians and the stock market.

In trying to bottom pick, we pick durians from the ground. Just don't stand under the durian tree too often; we might get knocked by the thorny durians on the way down...

In value investing, people scrutinize the business, it's financials, and it's valuations. Same for durians. If one wants to buy durians, he will scrutinize it, shake it, look at the color, look at the stem, check if the thorns are sharp and fresh. Lastly, having concluded that the durian is acceptable, we look at the price. Sometimes, durians are in large supply and we can get top grade durians at $10/kg. Sometimes, they are in short supply and cost $22/kg. So, we make a decision based on the current valuation whether to buy. If one deems it to be a value buy, we buy it at whatever Mr. Durian Seller/Mr. Market offers to us. If not, we just walk away, our banknotes safe and sound in our pockets.

We also can shop around. Stall A might be famous for it's Mao Shan Wang, but what if one wants to eat D24? Do we blindly go to Stall A? Sometimes, Stall B, which might not be famous for any cultivar, might offer D24 at cheaper prices. Same thing, we must also shop around for whoever lowers our cost. Sometimes, Stall A customers look down on Stall B customers because Stall B doesn't have a reputation. But, what matters is just the quality of the durians, no? Whether Stall A gives you aircon, more friendly staff, does it matter? I detect alot of snobbery and people turning their noses up at Standard Chartered Bank's offer of 0.20% commission with no minimum. Even though SCB might carry a bigger advantage for small players, people actually will save more when they trade more. If I want to buy $40,000 worth of ST Engineering, my commission for a traditional broker is at 0.275% which is $110+ gst. For SCB, that will be 0.20% which is $80+ gst. Of course, there are many other factors to look into; but I feel that the vibe of disdain and ridicule of SCB customers I get is unwarranted.

For durians, we must also know which cultivars are in season at the time we want to buy, which will offer us the best value for money. Say, in April, D24 from pahang is in season. We will get better value for money for D24 from Pahang in April, than say Mao Shan Wang from Perak. Sometimes, a flood/drought/whatever affects the whole South East Asia region and all durian trees, no matter how good, churn out poor quality durians. Same thing, we should look at the macro events and not just the business fundamentals of a stock. No matter how good a business is, a rising tide lifts all ships, and vice versa, a sinking tide grounds all ships. Even if a company is getting exceptional economic moat, ROE, ROI etc etc, a global economic downturn will sink it's stock price, will it not?

After all is said and done, when we bring the durian back, no matter how good it looked before we opened it, after opening, if there are worms inside, do we hold on to the durian hoping the worm will magically disappear, or do we take decisive action to throw the durian away before the worm replicates and goes into our other durians, or start to affect us?

That's my parallel of durian eating and stock picking. Enjoy both eating durians and picking stocks. Cheers!

Sunday, June 19, 2011

$20 approx per block of 1,000 KrisFlyer Miles via HSBC Credit Cards

HSBC Credit Cards have a promotion whereby:

The new HSBC rewards programme allows cardholders to purchase Rewards Points in blocks of 1,000. Every 2,500 Rewards Points = 1,000 KrisFlyer Miles.

HSBC allow cardholders to purchase 1,000 Rewards Points for S$8.

2,500 Rewards Points= 1,000 KF Miles= $20.

There is also a S$42.80 annual mileage transfer fee.

Essentially, you get to travel at discounts over SIA's published rates.

Award Tickets are also more flexible. You are able to change dates, flights, so long as the flight change is a same tier city (e.g. 29,750 KF Miles gets you one way to London, Manchester, Paris, Milan-Malpensa etc)

Take for example,

SIN-LHR ex. SIN:

Flexi Ticket: $1,710 + $683 taxes/surcharges = S$2393.40

Award Ticket: 60,000 KF Miles (after 15% online discount) = $1,200 + $683= $1,883

SIN-LAX ex. SIN

Flexi Ticket: $1,900 + $827 taxes/surcharges= S$2727

Award Ticket: 60,000 KF Miles (after 15% online discount) = $1,200 + $827= $2027

A great deal, in my opinion!

The new HSBC rewards programme allows cardholders to purchase Rewards Points in blocks of 1,000. Every 2,500 Rewards Points = 1,000 KrisFlyer Miles.

HSBC allow cardholders to purchase 1,000 Rewards Points for S$8.

2,500 Rewards Points= 1,000 KF Miles= $20.

There is also a S$42.80 annual mileage transfer fee.

Essentially, you get to travel at discounts over SIA's published rates.

Award Tickets are also more flexible. You are able to change dates, flights, so long as the flight change is a same tier city (e.g. 29,750 KF Miles gets you one way to London, Manchester, Paris, Milan-Malpensa etc)

Take for example,

SIN-LHR ex. SIN:

Flexi Ticket: $1,710 + $683 taxes/surcharges = S$2393.40

Award Ticket: 60,000 KF Miles (after 15% online discount) = $1,200 + $683= $1,883

SIN-LAX ex. SIN

Flexi Ticket: $1,900 + $827 taxes/surcharges= S$2727

Award Ticket: 60,000 KF Miles (after 15% online discount) = $1,200 + $827= $2027

A great deal, in my opinion!

Thursday, June 16, 2011

Cut Loss on CapitaLand and CapMallsAsia: Reflections and what's next

I cut loss on Capitaland and CapMallsAsia this week. Capitaland at 2.82, CMA at 1.53.

I am not disappointed with myself for losing money; what really irked me was my lack of a cut loss plan.

Trading with limited capital; you have to take losses quickly and enter trades only when risk reward ratio is good. (i.e., buying at support, cutting immediately when it's breached, having a reasonable profit target).

I learnt two important lessons from these two trades.

Start off with CMA.

CMA was a short term trade. I bought it, hoping to make a quick profit in the short run.

Bought close to support, 1.71, and support was at 1.68 at that time. Didn't cut until all the way till CMA breached it's 52-week low.

My earlier (losing) trades on Wilmar and NOL this yr, I cut loss 10c off and 2c off my purchase price respectively. Why? Bought close to support, when it was breached, quickly take losses.

This trade, I didnt have a cut loss plan and just blindly held on, thinking "it'll go up...it'll go up". Eventually, cut loss when the pain was too painful to bear.

For Capitaland, I bought it for 2 reasons: I thought it was fundamentally okay, I thought valuation was cheap. Fair enough.

I also bought it close to support of 3.08-3.11 at that time. (I bought at 3.15)

I didn't have a cut loss target for this- I made a fatal error in telling myself that Capitaland was for the long term, and I didn't have to have a stop loss.

The slew of bad news coming from MND and the Chinese Government is also bound to depress stock price across the board for property; I should have seen this.

Price is what we pay and Value is what we get. Cheap became cheaper. One advice I took to heart: "You can buy if it's cheap and reversing. You ALSO can buy if it's not cheap but going up. What you CANNOT do is to buy if it's cheap BUT not reversing."

Looking at the charts, I might have cut loss RIGHT at the bottom. CPL is at channel support and is likely to bounce off. Oh well, what's done is done.

That's my reflection. So what's next for me?

I've been on quite the losing streak; I think I've cut loss in my last 4 or 5 trades. All losses have been inconsequential except the CMA loss, and to a smaller extent, CPL. That was because I kept strictly to my cut loss rules. (Interestingly enough, all the stocks which I cut loss are trading at lower levels than where I cut them.) I will take a step backwards now, if there's a trade with high risk reward ratio (e.g. buying right at support and being able to cut within 2-3c, with price target of 10c), I will consider; if not, it'll be a time to cool off, observe the market and see where I went wrong.

I've had people advising me that with small capital, it's just not worth it to chase the 3-10% appreciation you typically get on your average trade. After all, 10% of $10,000 is just $1,000.

What people have been advising me to do, and which I think makes sense, is to wait for a huge correction, and then start buying slowly. (And sell slowly)

I'll take this period of time to think. A correction is underway, maybe there will be good bargains soon.

I am not disappointed with myself for losing money; what really irked me was my lack of a cut loss plan.

Trading with limited capital; you have to take losses quickly and enter trades only when risk reward ratio is good. (i.e., buying at support, cutting immediately when it's breached, having a reasonable profit target).

I learnt two important lessons from these two trades.

Start off with CMA.

CMA was a short term trade. I bought it, hoping to make a quick profit in the short run.

Bought close to support, 1.71, and support was at 1.68 at that time. Didn't cut until all the way till CMA breached it's 52-week low.

My earlier (losing) trades on Wilmar and NOL this yr, I cut loss 10c off and 2c off my purchase price respectively. Why? Bought close to support, when it was breached, quickly take losses.

This trade, I didnt have a cut loss plan and just blindly held on, thinking "it'll go up...it'll go up". Eventually, cut loss when the pain was too painful to bear.

For Capitaland, I bought it for 2 reasons: I thought it was fundamentally okay, I thought valuation was cheap. Fair enough.

I also bought it close to support of 3.08-3.11 at that time. (I bought at 3.15)

I didn't have a cut loss target for this- I made a fatal error in telling myself that Capitaland was for the long term, and I didn't have to have a stop loss.

The slew of bad news coming from MND and the Chinese Government is also bound to depress stock price across the board for property; I should have seen this.

Price is what we pay and Value is what we get. Cheap became cheaper. One advice I took to heart: "You can buy if it's cheap and reversing. You ALSO can buy if it's not cheap but going up. What you CANNOT do is to buy if it's cheap BUT not reversing."

Looking at the charts, I might have cut loss RIGHT at the bottom. CPL is at channel support and is likely to bounce off. Oh well, what's done is done.

That's my reflection. So what's next for me?

I've been on quite the losing streak; I think I've cut loss in my last 4 or 5 trades. All losses have been inconsequential except the CMA loss, and to a smaller extent, CPL. That was because I kept strictly to my cut loss rules. (Interestingly enough, all the stocks which I cut loss are trading at lower levels than where I cut them.) I will take a step backwards now, if there's a trade with high risk reward ratio (e.g. buying right at support and being able to cut within 2-3c, with price target of 10c), I will consider; if not, it'll be a time to cool off, observe the market and see where I went wrong.

I've had people advising me that with small capital, it's just not worth it to chase the 3-10% appreciation you typically get on your average trade. After all, 10% of $10,000 is just $1,000.

What people have been advising me to do, and which I think makes sense, is to wait for a huge correction, and then start buying slowly. (And sell slowly)

I'll take this period of time to think. A correction is underway, maybe there will be good bargains soon.

Wednesday, June 15, 2011

STI Components: Diving Contest?

I had an interesting discussion this afternoon on the cbox today about all stocks diving in SGX. One of the worst performers today was Neptune Orient Lines. As we like to say on the cbox, NOL has diversified into building submarines. :P

I think this song is pretty apt for what is happening now:

Being bored at work, I took the liberty to see the worst performing STI components over the past 52-weeks, these are the results for the STI diving contest:

Winner: CapMallsAsia. 52-week high: 2.33 Close: 1.46

Representing a dive of 37.33%

1st Runner Up: Neptune Orient Lines. 52-week high: 2.40 Close: 1.53

Representing a dive of 36.25%

2nd Runner Up: Capitaland. 52-week high: 4.23 Close: 2.87

Representing a dive of 32.15%

Consolation Prizes:

Singapore Exchange. 52-week high: 10.26 Close: 7.28

Representing a dive of 29.05%

City Developments. 52-week high: 13.62 Close: 10.42

Representing a dive of 23.50%

Wilmar. 52-week high: 6.93 Close: 5.42

Representing a dive of 21.8%

Ouch! This isn't a contest anyone wants to win.

Empathize with all who are stuck with these stocks. Am waiting to get rid of Capitaland; already got rid of CapitaMallsAsia at 1.50+. OUCH!

Thursday, June 9, 2011

Dapai International- YET ANOTHER fund raising exercise.

Dapai International, a counter which I used to have and divested at a loss, has had an SGX annoucement here stating the 1 for 4 rights issue.

Dapai will be issuing new shares at $0.080 apiece, and the reason for it is

"the entire amount of the Net Proceeds of S$19.3 million for financing in part the potential

acquisition of a suitable target in the backpack and luggage business segment which the

Company is currently negotiating, or if the potential acquisition being unsuccessful, the entire amount of the Net Proceeds of

S$19.3 million will be used for the Group’s future expansion of sales and distribution

networks and channels as well as general working capital purposes."

I have to thank Heavens that I divested immediately after I felt something not right with this company. My reasons at that time here.

This Rights Issue is yet another reason to be wary of this company.

Dapai has a cash horde of over S$100,000,000, with negligible debt. Yet, it still begs shareholders for a mere S$19,300,000. In the words of Nick: " It is like a man who claims to have $100 in his pocket but need to beg for $19 to buy his favourite bag lol"" "

Look at the part of the SGX annoucement I bolded. Essentially, what Dapai is telling you is, should he fail to secure stock of his favorite bag, he will just keep the money in his wallet, thanks for your generosity :)

I emailed the IR in March 2011 to enquire why they did not pay a dividend. The IR replied they needed the cash for it's working capital. Yet, still need to beg shareholders for money again? Huh? Wu yiah bo?

{kind=link}

Dapai will be issuing new shares at $0.080 apiece, and the reason for it is

"the entire amount of the Net Proceeds of S$19.3 million for financing in part the potential

acquisition of a suitable target in the backpack and luggage business segment which the

Company is currently negotiating, or if the potential acquisition being unsuccessful, the entire amount of the Net Proceeds of

S$19.3 million will be used for the Group’s future expansion of sales and distribution

networks and channels as well as general working capital purposes."

I have to thank Heavens that I divested immediately after I felt something not right with this company. My reasons at that time here.

This Rights Issue is yet another reason to be wary of this company.

Dapai has a cash horde of over S$100,000,000, with negligible debt. Yet, it still begs shareholders for a mere S$19,300,000. In the words of Nick: " It is like a man who claims to have $100 in his pocket but need to beg for $19 to buy his favourite bag lol"" "

Look at the part of the SGX annoucement I bolded. Essentially, what Dapai is telling you is, should he fail to secure stock of his favorite bag, he will just keep the money in his wallet, thanks for your generosity :)

I emailed the IR in March 2011 to enquire why they did not pay a dividend. The IR replied they needed the cash for it's working capital. Yet, still need to beg shareholders for money again? Huh? Wu yiah bo?

Sunday, June 5, 2011

Standard Chartered Bank Singapore- NO MINIMUM BROKERAGE FEES!

SCB Singapore has a new i-banking cum brokerage system where you can enjoy NO MINIMUM brokerage fees. The catch is:

-No Contra. You have to have the cash in your Securities account before they allow you to key in your order. However, settlement for SGX is still done in T+3. Not a problem for those who are investing with money they have. Only a problem for those who contra beyond their means.

-Your shares will be kept in SCB Nominees. This subjects you to the counterparty risk of SCB failing; which I think is pretty remote. There are no custodian fees.

EDIT: I've been informed that even if SCB does fail; the legal and equitable titles are still ours; the shares will still belong to us should SCB Nominees fail.

-0.20% for SGX shares and 0.25% for NYSE, NASDAQ, Paris Bourse, Deutsche Boerse, London Stock Exchange, Swiss Stock Exchange, Tokyo Stock Exchange, Australian Stock Exchange, Amsterdam Stock Exchange etc. Notably absent is the Bursa Malaysia.

I am very excited with the prospect of being able to invest outside of Singapore at very cheap rates.

I am also very excited with the prospect of being able to do Dollar Cost Averaging on stocks which I think are at good prices, one lot by one lot, since I do not have a high capital. (e.g. Sabana REIT and PohTC)

Lastly I am excited with the prospect of being able to practice my TA with small lots. e.g. I can buy 1 lot of, say, Noble Group if I believe it's TA signals are good. This, I believe, is better than paper trading (which I think is useless, by the way) and better than risking a large portion of my capital, since I still am at the learning stage.

An example of brokerage fees:

1 lot of PohTC- 40c ($400)- commission: 80c

1 lot of Noble Group Ltd- $2.00 ($2000)- commission: $4

Obviously for the people who trade with minimum $10,000 each time, this is not a big breakthrough but for small fry like me, this is a very exciting prospect.

I will be going down to the Battery Road Branch tomorrow during lunchtime to apply.

The Old Boy's

Wednesday, June 1, 2011

May 2011 Portfolio Updates/Summary

May 2011 was yet another uneventful month for me, as I count the months left till university starts (3). Have been working as a temporary staff in one of the banks at CBD area.

Used my iPhone to buy a stock for the first time.

Also received many dividends this month, from ST Engg, First REIT, MIT and PohTC.

Added two new counters to my portfolio: CapMallsAsia and Capitaland.

Capitaland is a value buy, with NTA and NAV both at $3.20-ish.

CapMallsAsia, however, is a trade. Unfortunately it has been very bearish recently, going down all the way to $1.58 until recovering to $1.63 today. Will divest at resistance of $1.68 if tested.

My other counters have been very weak after going XD. ST Engg especially, dropping from $3.30 to $2.97, though dividend was only 11.5cents. PohTC dropped from 45c to 40c despite a small dividend of 2c.

The best performer is First REIT, going from 75c to 79c. It has been included into the MSCI Singapore Index as of today (SiMSCI). Read more about it at AK's blog here.

Sabana REIT has also been added to MSCI Global Small Caps. Read more here.

Portfolio is still green, due to my dividends and capital gain over the past year from ST Engineering, and the good performace of First REIT.

YTD is red due to CMA, my multiple trades that went awry (NOL, Wilmar).

Used my iPhone to buy a stock for the first time.

Also received many dividends this month, from ST Engg, First REIT, MIT and PohTC.

| Stock Bought | Buy Price | Market Price | P/L not incl. Dividend |

| MIT | $0.930 | $1.17 | 25.81% |

| Sabana | $1.050 | $0.94 | -10.48% |

| First REIT | $0.700 | $0.79 | 12.86% |

| ST Engineering | 2++ (Average) | $2.97 | Not Available |

| Poh Tiong Choon Log | $0.48 | $0.40 | -16.67% |

| Capitaland | $3.15 | $3.11 | -1.27% |

| CapMallsAsia | $1.71 | $1.63 | -4.68% |

Added two new counters to my portfolio: CapMallsAsia and Capitaland.

Capitaland is a value buy, with NTA and NAV both at $3.20-ish.

CapMallsAsia, however, is a trade. Unfortunately it has been very bearish recently, going down all the way to $1.58 until recovering to $1.63 today. Will divest at resistance of $1.68 if tested.

My other counters have been very weak after going XD. ST Engg especially, dropping from $3.30 to $2.97, though dividend was only 11.5cents. PohTC dropped from 45c to 40c despite a small dividend of 2c.

The best performer is First REIT, going from 75c to 79c. It has been included into the MSCI Singapore Index as of today (SiMSCI). Read more about it at AK's blog here.

Sabana REIT has also been added to MSCI Global Small Caps. Read more here.

Portfolio is still green, due to my dividends and capital gain over the past year from ST Engineering, and the good performace of First REIT.

YTD is red due to CMA, my multiple trades that went awry (NOL, Wilmar).

Saturday, May 21, 2011

Money changers in Raffles Place

|

| My attempt at doing something artistic! |

I recently went to the Arcade to change more Pounds Sterling, since the exchange rate was favorable.

The Arcade is FULL of money changers, presumably with better rates for different currencies.

For example, the money changer I queued up for had at least 20 people ahead of me, and most were changing Thai Baht, Ringgit, Chinese Renminbi.

The spreads on offer are really low and competitive. These money changers obviously make money through volume.

Take Pounds Sterling as an example.

Spot Rate was S$2.0040 to £1.00 at the time when I was changing.

UOB preferential staff rates were $1.9950 buy and $2.0090 sell (70 pip spread)

The money changer I went to, the rate was $1.9970 buy and $2.0140 sell (85 pip spread)

Essentially, they make about $10 for every £1,000 you change.

The spread for US dollar was even smaller!

The queue was REALLLY long! I queued up at 12.05pm and was attended to only at 12.25pm. People really love changing their money and going overseas don't they?

Wednesday, May 11, 2011

I am a new Capitaland shareholder.

As per my previous post here, I was contemplating buying Capitaland as a value buy. I put an order yesterday and today to buy capitaland at $3.13 and $3.15. Well, the $3.15 order was filled and I am a new capitaland shareholder.

My reasons for purchasing this security has been covered in the previous post.

On the technical side, Capitaland fell on extremely heavy volume today, apparently on fears that there will be policy tightening in China and Singapore (link here). Yet, it did manage to recover 3c from it's low to close at $3.17.

the counter-party for my shares was Merrill Lynch, honestly not too comfortable with that, it indicates BBs selling the share.

I've bought close to support at $3.12. This should be a good thing.

My reasons for purchasing this security has been covered in the previous post.

On the technical side, Capitaland fell on extremely heavy volume today, apparently on fears that there will be policy tightening in China and Singapore (link here). Yet, it did manage to recover 3c from it's low to close at $3.17.

the counter-party for my shares was Merrill Lynch, honestly not too comfortable with that, it indicates BBs selling the share.

I've bought close to support at $3.12. This should be a good thing.

Tuesday, May 10, 2011

Bought CapitaMalls Asia today.

As per my previous post here, I've kept my eyes on three counters. The two commodity counters have since risen. I will still keep a lookout if they do reach my purchase price target again; if not, there will always be other trading opportunities.

I did, however, buy CMA today at $1.71. Like I explained in the previous post, CMA is at support at $1.70. Buying at support is a good idea.

Indicators show oversold condition for MACD and stochastics.

Indicators show oversold condition for MACD and stochastics.

There was also muted selling today.

Immediate resistance is at $1.78 should CMA have a bullish inclination, and that is where I will sell CMA off. Should CMA see high volume breaking of that resistance, I will sell off at the next resistance at $1.84.

Breaking of $1.70 support will see downside toward $1.66. Should prices drop below $1.66 at high volume, I will cut loss.

I did, however, buy CMA today at $1.71. Like I explained in the previous post, CMA is at support at $1.70. Buying at support is a good idea.

There was also muted selling today.

Immediate resistance is at $1.78 should CMA have a bullish inclination, and that is where I will sell CMA off. Should CMA see high volume breaking of that resistance, I will sell off at the next resistance at $1.84.

Breaking of $1.70 support will see downside toward $1.66. Should prices drop below $1.66 at high volume, I will cut loss.

Sunday, May 8, 2011

Quick thoughts on Capitaland

Capitaland deals with...what else? Real Estate.

I'm bullish on real estate in Singapore especially, with the PAP government's constant influx of foreigners into Singapore. (I'm not going to debate the merits of this policy; this is an investment blog.)

What then is the direction of prices of real estate? only one way, I feel.

Might as well buy a company that will benefit from this policy.

Hence, I'm looking into adding Capitaland into my stable of long term holdings.

I'm not an accountant, I can't read financial statements that well. Yet, the fact that Temasek owns almost 40% of this company gives me confidence. (Same reason why I invested in ST Engineering.)

Follow what the BBs are investing in...and the biggest BB in Singapore is none other than Temasek...

Capitaland's NAV is currently at 327c and NTA is at 316c.

For property stock, I think the NTA is more appropriate than NAV.

Capitaland is currently trading at $3.26 with a CD of $0.06. Logically, it should drop to $3.20 upon XD, but the recent trend has been counters dropping more than their dividend amount.

Let's see where would be a good place to buy, using charts:

This was also the 52 week low.

Since Capland will be going XD next week, technically prices should fall to 320c.

Yet given the bearish bent to the market these couple of weeks, prices may fall further past it's dividend amount (just like ST Engg, SembMarine, SCI, Wilmar inter alia). A good price to get it might be around the 311c to 318c area next week.

Thursday, May 5, 2011

Trading Ideas: Noble, GAR, CMA

Noble:

Dropped on high volume today despite having a new SWF buying over 50,000,000 units of Noble Group.

Strong support seen at $1.98 to $2.00 region, which coincidentally coincides with the lower channel line.

This one looks good. I will enter should prices drop to that region.

Golden Agri:

Another counter close to a strong support.

Strong support eyed at 63c.

Seems to be consolidating around 65c level.

Will consider entering should prices weaken to 63c

CapitaMallsAsia:

this one is another close to support.

this one is another close to support.

Indicators wise, all three counters paint a similar picture:

- declining MACD, the latter two in negative region whilst Noble in positive region

-Bullish divergence for force index

-oversold stochastics.

Of these three, Noble looks the most compelling should it reach it's target price (Longer term picture is of an uptrend as opposed to downtrend for CMA). I will revisit them again if they reach target price...

Dropped on high volume today despite having a new SWF buying over 50,000,000 units of Noble Group.

Strong support seen at $1.98 to $2.00 region, which coincidentally coincides with the lower channel line.

This one looks good. I will enter should prices drop to that region.

Golden Agri:

Another counter close to a strong support.

Strong support eyed at 63c.

Seems to be consolidating around 65c level.

Will consider entering should prices weaken to 63c

CapitaMallsAsia:

Indicators wise, all three counters paint a similar picture:

- declining MACD, the latter two in negative region whilst Noble in positive region

-Bullish divergence for force index

-oversold stochastics.

Of these three, Noble looks the most compelling should it reach it's target price (Longer term picture is of an uptrend as opposed to downtrend for CMA). I will revisit them again if they reach target price...

Monday, May 2, 2011

APRIL 2011 Portfolio Updates

The month of April 2011 was uneventful.

Quick updates:

ST Engineering: No annoucements last month except for a $320 million contract secured by ST Aerospace.

More revenue which is good...

Went XD last week, so I will be receiving my 11.55c per share dividend this month.

Was trading at $3.25 during CD and now at $3.15 during XD.

Poh Tiong Choon Logistics:

No annoucements, all resolutions passed at the AGM. Didn't manage to go for the AGM held at Jurong Country Club as I had work.

Insiders are still buying in, indicating to me they have confidence in the business.

2c Dividend, going XD soon.

Sabana REIT:

First payout is at 3cents, in line with projections. Note that 3c is from listing date end Nov to 31/3/2011, making it a payout for FOUR months, which is why it is higher.

First REIT:

Went XD last week, with a payout of 1.58c in line with projections.

No Annoucements made.

All in all, with the dividends received and the recent market recovery, my portfolio has returned to a profit.

May looks to be a good month with payouts coming from all 4 of my counters.

My investments, ranked by market price, are:

1.) ST Engg

2.) First REIT

3.) PohTC

4.) Sabana

Quick updates:

ST Engineering: No annoucements last month except for a $320 million contract secured by ST Aerospace.

Went XD last week, so I will be receiving my 11.55c per share dividend this month.

Was trading at $3.25 during CD and now at $3.15 during XD.

Poh Tiong Choon Logistics:

No annoucements, all resolutions passed at the AGM. Didn't manage to go for the AGM held at Jurong Country Club as I had work.

Insiders are still buying in, indicating to me they have confidence in the business.

2c Dividend, going XD soon.

Sabana REIT:

First payout is at 3cents, in line with projections. Note that 3c is from listing date end Nov to 31/3/2011, making it a payout for FOUR months, which is why it is higher.

First REIT:

Went XD last week, with a payout of 1.58c in line with projections.

No Annoucements made.

All in all, with the dividends received and the recent market recovery, my portfolio has returned to a profit.

May looks to be a good month with payouts coming from all 4 of my counters.

My investments, ranked by market price, are:

1.) ST Engg

2.) First REIT

3.) PohTC

4.) Sabana

Saturday, April 30, 2011

Potential Short Term Trade: Golden Agri

{kind=link}

We can see that GAR is on a long term uptrend, and hence, two choices here: trade from long side or step aside.

I will choose to go long on GAR, explained on the daily:

We shall look at the indicators first:

The Force Index (Long Term) shows a nice bullish divergence, indicating lack of power in pushing the price down.

The MACD lines show no divergence, they rise as price rise.

The RSI also show no divergence.

Stochastics show a deeply oversold condition.

However, oversold can remain oversold for a long time. Just look at Wilmar.

Indicators don't show any juicy bullish divergences, yet what I like about this potential trade:

1.) GAR is very close to it's strong support at 65c. Look at the line I drew.

2.) When GAR was bullish in 2009 and 2010, it bounced from value zone to upper channel line. Likewise, when GAR was bearish this year, it bounced between value zone and lower channel line.

Looking at the chart now, GAR is slightly below the value zone. I daresay we've resumed the bullish trend of STI now. Hence, prices should trade between upper channel line and value zone, in a uptrend.

Target Entry Price for this trade: 65c to 66c

Profit Taking target for this trade: Midpoint between Upper channel line and value zone @ 70c to 71c

Stop Loss: 61c, though I don't expect it to go there.

Thursday, April 21, 2011

How I almost got conned into buying a "savings product" from an insurance agent

Writing this post after quite a debate on ILP on La Papillon's chatbox.

Back in late 2010, when I was fresh to the stock market and unused yet to the intricacies of finance, I was approached at Harborfront MRT by one of those people who asked me whether I'd have time to fill up a survey form. I did, and this was how the saga panned out.

The survey form has a few questions, some of which I could remember are:

1.) What is your monthly income?

Isaac's Selection: $500 to $1000 ( I was an NSF at that time)

2.) Which banks do you use?

Isaac's Selection: Citibank and POSB

3.) Are you aware that there are products out there with higher interest rates than what you can get in banks?

Isaac's Selection: No

At that point, the agent came out and did a sales pitch, briefly:

1.) We can offer you >3% (cue the :o face here) per annum! With just a minimum of $80 a month investment!

2.) We can let you take out $200 per annum ( :o again) after the first two years!

I then asked her what company was this from. I shall not reveal it here, suffice to say it is a big listed international insurance company.

I was pretty intrigued (didn't know about bonds, REITs and stuff back then) and decided to leave my cellphone number with her. It helped that she was willing to travel to near my army camp to discuss it further.

A week later, we did meet up near my camp, during my lunchtime. (which was 2 hours. I love the army)

She discussed it with me and mentioned there are 2 options. 15 year and 25 year redemption period. I was pretty shocked, for the time period was extremely long. She also did up one of those computerised quotes for me.

The gist of it was:

-I was to pay them $78 a month, for the next 25 years. Total of $23,400

-There will be death cover of $25,000 and some minor illness cover, of which i was to pay $3 a month. (The investment portion was thus $75 a month).

-ASSUMING I was to NOT take any cash out from this policy for the next 25 years, my payout was to be about $28,000 to $30,000 in the year 2035.

-There might be some increase in payout ratio if they had a good year.

-Essentially, my best case scenario was to get back $31,000 in 2025, worst case $28,000. Now, what is the compounded interest for that? Roughly but less than 2%!

Hey! I thought I was promised 3% at the MRT station?

Taking a closer look at the policy, the amount used to pay for the administrative charges and commissions was a whopping $1,500! :o face from me now!

That's over 6% of the total policy injection into the agent's pocket!

And she didn't even buy coffee for me! (She bought for herself!)

I emailed her back and mentioned that I would not be taking up the policy for it provided me with useless coverage ($25,000 compared with the $400,000 I have now from SAF Aviva and the compulsory $25,000 from CPF and another $100,000 term insurance my parents bought) and poor returns.

She was very persistent and reminded me that this policy "beri good wans...give you protection and investment leh! Pruss so cheap leh! $78 a month nia! "

Erm...I thought you pitched this as a pure investment policy?

When I replied that SGS Bonds gave about the same yield(my father told me) , she mumbled something about the risk involved with equities!

Lesson Learnt: Do you own due diligence!

Back in late 2010, when I was fresh to the stock market and unused yet to the intricacies of finance, I was approached at Harborfront MRT by one of those people who asked me whether I'd have time to fill up a survey form. I did, and this was how the saga panned out.

The survey form has a few questions, some of which I could remember are:

1.) What is your monthly income?

Isaac's Selection: $500 to $1000 ( I was an NSF at that time)

2.) Which banks do you use?

Isaac's Selection: Citibank and POSB

3.) Are you aware that there are products out there with higher interest rates than what you can get in banks?

Isaac's Selection: No

At that point, the agent came out and did a sales pitch, briefly:

1.) We can offer you >3% (cue the :o face here) per annum! With just a minimum of $80 a month investment!

2.) We can let you take out $200 per annum ( :o again) after the first two years!

I then asked her what company was this from. I shall not reveal it here, suffice to say it is a big listed international insurance company.

I was pretty intrigued (didn't know about bonds, REITs and stuff back then) and decided to leave my cellphone number with her. It helped that she was willing to travel to near my army camp to discuss it further.

A week later, we did meet up near my camp, during my lunchtime. (which was 2 hours. I love the army)

She discussed it with me and mentioned there are 2 options. 15 year and 25 year redemption period. I was pretty shocked, for the time period was extremely long. She also did up one of those computerised quotes for me.

The gist of it was:

-I was to pay them $78 a month, for the next 25 years. Total of $23,400

-There will be death cover of $25,000 and some minor illness cover, of which i was to pay $3 a month. (The investment portion was thus $75 a month).

-ASSUMING I was to NOT take any cash out from this policy for the next 25 years, my payout was to be about $28,000 to $30,000 in the year 2035.

-There might be some increase in payout ratio if they had a good year.

-Essentially, my best case scenario was to get back $31,000 in 2025, worst case $28,000. Now, what is the compounded interest for that? Roughly but less than 2%!

Hey! I thought I was promised 3% at the MRT station?

Taking a closer look at the policy, the amount used to pay for the administrative charges and commissions was a whopping $1,500! :o face from me now!

That's over 6% of the total policy injection into the agent's pocket!

And she didn't even buy coffee for me! (She bought for herself!)

I emailed her back and mentioned that I would not be taking up the policy for it provided me with useless coverage ($25,000 compared with the $400,000 I have now from SAF Aviva and the compulsory $25,000 from CPF and another $100,000 term insurance my parents bought) and poor returns.

She was very persistent and reminded me that this policy "beri good wans...give you protection and investment leh! Pruss so cheap leh! $78 a month nia! "

Erm...I thought you pitched this as a pure investment policy?

When I replied that SGS Bonds gave about the same yield(my father told me) , she mumbled something about the risk involved with equities!

Lesson Learnt: Do you own due diligence!

Sunday, April 17, 2011

Hyflux Preference Shares

Hyflux is offering S$200 million worth of Cumulative Non-Convertible preference shares at 6% p.a.

Cumulative in that if they do not pay you this time, they have to pay you the next time around. They will also recall the shares at par value in 2018, failing which, they will step up to 8%.

Pros of this:

1.) High yield in a currency with historically low interest rates.

2.) 8% if they do not recall the shares in 2018.

3.) If price opens high, can stag off for quick profit

Cons:

1.) Hyflux is a terribly cyclical company, may face difficulty paying out the dividends during bad times; having said that, the cumulative portion guarantees 6%, just not the timing

2.) Hyflux's equity is lower than liabilities.

3.) Why did they need to find financing at 6%, unless banks are reluctant to lend them more money?Concerned with their balance sheet, they only are willing to lend at a high interest rate?

4.) SPH and Starhub have close to 6% dividend yield. Having said that, SPH/SH do not guarantee this high payout.

I won't be applying for this CPS. minimum bid is at $10,000, i can only afford to bid $10,000. Probably just going to waste $2.

Cumulative in that if they do not pay you this time, they have to pay you the next time around. They will also recall the shares at par value in 2018, failing which, they will step up to 8%.

Pros of this:

1.) High yield in a currency with historically low interest rates.

2.) 8% if they do not recall the shares in 2018.

3.) If price opens high, can stag off for quick profit

Cons:

1.) Hyflux is a terribly cyclical company, may face difficulty paying out the dividends during bad times; having said that, the cumulative portion guarantees 6%, just not the timing

2.) Hyflux's equity is lower than liabilities.

3.) Why did they need to find financing at 6%, unless banks are reluctant to lend them more money?Concerned with their balance sheet, they only are willing to lend at a high interest rate?

4.) SPH and Starhub have close to 6% dividend yield. Having said that, SPH/SH do not guarantee this high payout.

I won't be applying for this CPS. minimum bid is at $10,000, i can only afford to bid $10,000. Probably just going to waste $2.

Saturday, April 16, 2011

Some Travel Lobangs for those interested

All fares are all in.

Singapore to Melbourne on Royal Brunei Airlines @ $631. Ongoing promotion to celebrate their new port-of-call at Melbourne.

Fly from Singapore to Bandar Sri Begawan, then to Melbourne.

Singapore to New York City on Delta Airlines @ $920. Book till end of April for outbound travel to June. Not available on Delta's website, but available with travel agents like Zuji, STA Travel and Mustafa.

Fly from Singapore to Narita and then on to John F. Kennedy Airport.

Singapore to Sydney on Garuda @ $800. Outbound travel all the way till August. Again, not available on their own site but available with travel agents like Zuji, Mustafa and STA.

Fly from Singapore to Ngurah Rai Airport (Bali) on a codeshare with SQ on SQ equipment, then on to Sydney on Garuda. Return from Sydney to Jakarta and then on to Singapore, all sectors on Garuda.

Singapore to Melbourne on Royal Brunei Airlines @ $631. Ongoing promotion to celebrate their new port-of-call at Melbourne.

Fly from Singapore to Bandar Sri Begawan, then to Melbourne.

Singapore to New York City on Delta Airlines @ $920. Book till end of April for outbound travel to June. Not available on Delta's website, but available with travel agents like Zuji, STA Travel and Mustafa.

Fly from Singapore to Narita and then on to John F. Kennedy Airport.

Singapore to Sydney on Garuda @ $800. Outbound travel all the way till August. Again, not available on their own site but available with travel agents like Zuji, Mustafa and STA.

Fly from Singapore to Ngurah Rai Airport (Bali) on a codeshare with SQ on SQ equipment, then on to Sydney on Garuda. Return from Sydney to Jakarta and then on to Singapore, all sectors on Garuda.

Wednesday, April 13, 2011

Why I won't subscribe to Mapletree Commercial nor buy HPH Trust

Simple reason.

Yield is at 5% for Mapletree Commercial. '

Yield is at 5% for HPH Trust, in a depreciating US Dollar.

DBS NCPS was offered at 4.7%.

Why bother taking on more risk for a poor return, when one can easily have gotten 0.3% less yield for a much better peace of mind with DBS NCPS?

Mapletree Commercial might make for a good stag, but I sure am not holding it for it's yield.

Yield is at 5% for Mapletree Commercial. '

Yield is at 5% for HPH Trust, in a depreciating US Dollar.

DBS NCPS was offered at 4.7%.

Why bother taking on more risk for a poor return, when one can easily have gotten 0.3% less yield for a much better peace of mind with DBS NCPS?

Mapletree Commercial might make for a good stag, but I sure am not holding it for it's yield.

Sunday, April 3, 2011

March 2011 Portfolio Update

Having liquidated my lone S chip- Dapai International with reasons here, my Long Term holdings now consist of only 5 stocks:

Comments:

MIT: At my buy price, 93c at IPO, gives close to an 8% yield + 12% capital gain at closing price of $1.05. Not divesting because: Reasonably high yield at my price and peace of mind from a strong parent. Even as CIT, First, Sabana and AIMSAMPIREIT give almost 10% yield at their price, I'm willing to accept a lower yield for MIT's "blue chip-ness", so to speak.

Sabana: 8.22% yield this year and 8.5% projected yield at my price, $1.05. 11% capital loss currently. At current prices, Sabana gives a 9.5% yield- highly attractive yet commensurately high with erstwhile troubled AIMSAMPIREIT and CIT. Not divesting, as I only have 1 lot, so will just chuck this into the freezer. Seeing heavy selling by BB's recently, having touched an all time low of 92c last week. AK71 of ASSI has a summary of Sabana here.

My first freezer stock..... :(

First REIT: Saw heavy selling during the Japanese crisis, has recovered somewhat but not to the fervour of January 2011 yet where it touched a high of 77c due to a highly favourable OCBC research report. Gives me a projected 9.5% yield at my buy price and also 5.5% capital gain YTD. Received a small dividend in Jan 2011.

Poh Tiong Choon Logistics: I bought this for pretty dumb reasons here and I probably suffer from confirmation bias now. Looking back, it was a POOR decision to buy at that point. Why? Look at the technicals at the time I bought. Way above the value zone. I was very "gian gian" to enter. Luckily for me, I didn't suffer too heavy a paper loss.

As for the fundamentals: PTC showed a pretty good 2H 2010 profit turnaround. Insiders are still buying and buying and providing a support at 43cents. I usually see 100 lots buy queue at 43cents everyday. 2cents dividend coming next month.

ST Engineering: A very blue blue chip, owned by our government. No need to say anything. 11.55cents coming in May. Nice capital appreciation for me too :)

May looks to be a good month: $400 coming from the government due to budget 2011, 11.55c a lot from ST engg, Sabana distribution, maybe First and MIT too.

| Stock Bought | Buy Price |

| MIT | $0.930 |

| Sabana | $1.050 |

| First REIT | $0.700 |

| ST Engineering | |

| Poh Tiong Choon Log | 0.48 |

Comments:

MIT: At my buy price, 93c at IPO, gives close to an 8% yield + 12% capital gain at closing price of $1.05. Not divesting because: Reasonably high yield at my price and peace of mind from a strong parent. Even as CIT, First, Sabana and AIMSAMPIREIT give almost 10% yield at their price, I'm willing to accept a lower yield for MIT's "blue chip-ness", so to speak.

Sabana: 8.22% yield this year and 8.5% projected yield at my price, $1.05. 11% capital loss currently. At current prices, Sabana gives a 9.5% yield- highly attractive yet commensurately high with erstwhile troubled AIMSAMPIREIT and CIT. Not divesting, as I only have 1 lot, so will just chuck this into the freezer. Seeing heavy selling by BB's recently, having touched an all time low of 92c last week. AK71 of ASSI has a summary of Sabana here.

My first freezer stock..... :(

First REIT: Saw heavy selling during the Japanese crisis, has recovered somewhat but not to the fervour of January 2011 yet where it touched a high of 77c due to a highly favourable OCBC research report. Gives me a projected 9.5% yield at my buy price and also 5.5% capital gain YTD. Received a small dividend in Jan 2011.

Poh Tiong Choon Logistics: I bought this for pretty dumb reasons here and I probably suffer from confirmation bias now. Looking back, it was a POOR decision to buy at that point. Why? Look at the technicals at the time I bought. Way above the value zone. I was very "gian gian" to enter. Luckily for me, I didn't suffer too heavy a paper loss.

As for the fundamentals: PTC showed a pretty good 2H 2010 profit turnaround. Insiders are still buying and buying and providing a support at 43cents. I usually see 100 lots buy queue at 43cents everyday. 2cents dividend coming next month.

ST Engineering: A very blue blue chip, owned by our government. No need to say anything. 11.55cents coming in May. Nice capital appreciation for me too :)

May looks to be a good month: $400 coming from the government due to budget 2011, 11.55c a lot from ST engg, Sabana distribution, maybe First and MIT too.

Wednesday, March 23, 2011

Sold NOL as I quickly cut loss.

I sold NOL off after less than a day.

A poor decision to enter.

why?

In an uptrend, resistance is usually provided by the higher moving average envelope (something like a straight Bollinger Band) and a good time to buy is usually at the value zone (the area around the 13 day EMA and 21 day EMA), and in a downtrend, support is provided by the lower moving average envelope and resistance at the value zone.

in other words, in uptrends, buy normalcy and sell mania. in downtrends, buy depression and sell normalcy.

I should have applied the latter to NOL this time.

Since this is a short term trade, what matters is the short term trend, which is down.

Undoubtedly, MACD histogram has a nice bullish divergence. Very nice in fact.

RSI and Stochastics have bullish divergence yet are capped at 50%.

Why I decided to sell:

1.) Volume rises on down days and drops on up days. Affirms that investors/traders are reluctant to push NOL up.

2.) I bought at the value zone. This would be ok were my intentions to keep NOL for long term. But, since my intention is to sell it off soon, and since the value zone acts as the major resistance in a downtrend, I bought at resistance. And that's suicidal.